by Carol H Cox

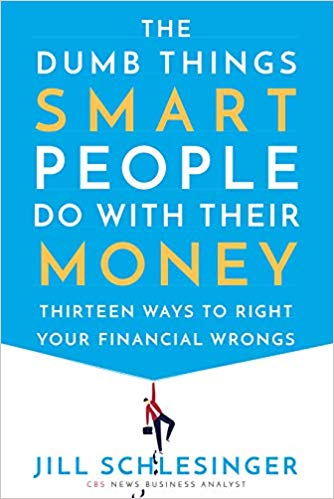

If you’ve ever listened to Jill Schlesinger’s podcast, you know that she’s a straight shooter, smart, and as to the point as you could wish for in a financial adviser. I really respect the woman and was excited to hear that she had a new book out, The Dumb Things Smart People Do With Their Money: Thirteen Ways to Right Your Financial Wrongs.

Because I love the way she banters on air and her manner of making me feel like she’s talking to me personally on her show, I decided to listen to the audiobook version, which she narrates herself. Great choice!

It’s an enjoyable, no holds barred dive into how not to make stupid mistakes with our money. If we’d only follow her advice, we’d no doubt be much better at such practices as investing using reason instead of emotion, avoiding obsessive emphasis on money, finding affordable ways to send kids to college, prioritizing retirement savings, and demystifying the allure of real estate, and so on.

Continue reading “Audiobook Recommendation: Jill Schlesinger’s New Personal Finance Book”

parent or grandparent considering co-signing on or taking out a student loan for your child or grandchild? Well, you may first want to read a new study on this matter.

parent or grandparent considering co-signing on or taking out a student loan for your child or grandchild? Well, you may first want to read a new study on this matter.